oleh admin | Agu 28, 2025 | banking, financial services, money, securities, technology

Published on, Aug. 19 — August 19, 2025 7:24 AM

The Central Bank of Pakistan (CBP), known as the State Bank of Pakistan (SBP), plans to introduce its enhanced payment and settlement platform named PRISM+ on Tuesday, August 19, 2025. The ceremony will be presided over by the Governor of the State Bank of Pakistan, Mr. Jameel Ahmad, with participation from high-ranking SBP personnel, delegates from banking entities, and important players within the finance industry. This development represents an essential step forward in the continuous improvement of Pakistan’s financial framework.

This innovative framework marks a significant advancement in updating the way funds and governmental assets circulate within the nation’s monetary network.

PRISM+ is based on the global ISO 20022 messaging standard, which is used in many advanced financial systems around the world. It includes two key components:

An improved Real-Time Gross Settlement (RTGS) system designed for swift processing of major transactions between involved parties

A completely new Central Securities Depository (CSD) responsible for handling government instruments like Treasury Bills, Public Investment Bonds, and additional government-related financial assets

What PRISM+ Provides: A Quicker and More Intelligent Banking System: PRISM+ introduces various innovative tools and functionalities for banks to enhance their everyday management processes:

Immediate transfer of significant transactions among users Choice to plan payments for a later day

Payment handling based on priority (key transactions are processed initially)

Real-time dashboards displaying account balances, outstanding payments, and transaction processing status

Automated computation of charges and bills

Enhanced Management of Sovereign Securities: The CSD within PRISM+ enables banks to purchase, trade, and oversee government bonds with greater ease:

Primary Market Auctions: Financial institutions may place offers and receive outcomes instantly

Trading in the Secondary Market: Financial institutions may send transaction orders, which are promptly paired and finalized.

Risk Administration: Financial institutions have the ability to monitor and assess their collateralized assets, as well as determine the amount that can be utilized.

Monetary Policy Tools: Assists the State Bank of Pakistan in adding or removing funds from the economy and facilitating immediate transaction settlements

Enhanced Visibility and Safety: Each transaction comes with a complete record of activity

Role-based access ensures only authorized users can perform actions

Real-time alerts notify banks about any issues with settlement

Innovative Solutions for Managing Cash Flow and Payments

Liquidity Saving Queues: To reduce delays and manage liquidity better, PRISM+ uses special queues:

High-priority payments are settled right away

Payments with lower priority are placed in distinct queues and processed in groups to prevent overcrowding.

Reserve Earmarking: Banks can set aside funds specifically for systems like Raast, 1Link, NIFT, or NCCPL. This makes sure critical transactions are not delayed due to general liquidity use.

Intraday Liquidity Facility (ILF): Financial institutions have the option to obtain temporary funding by pledging qualifying government bonds. This mechanism helps maintain seamless transactions despite temporary fund shortages.

Other Improvements

Longer operating hours for better access: Payment cancellation and return messages can now be handled in real time

Facility to deposit or withdraw cash at the SBP Karachi branch for specific transactions

The platform was created in accordance with SBP’s Vision 2028, seeking to build a contemporary, accessible, and strong financial environment. Comprehensive involvement of stakeholders during the creation phase has made sure that PRISM+ incorporates global standard approaches while addressing Pakistan’s specific market requirements.

oleh admin | Agu 19, 2025 | banking, economic policy, economics, monetary policy, politics and government

Published on, Aug. 19 — August 19, 2025 11:54 AM

The International Monetary Fund (IMF) has asked Pakistan to remove the finance secretary from the State Bank of Pakistan (SBP) board and immediately fill two vacant deputy governor positions to strengthen institutional independence.

The lender has also recommended amending the Banking Companies Ordinance of 1962 to remove the federal government’s authority to instruct SBP to inspect commercial banks, further reducing state influence over financial regulation.

In its Governance and Corruption Diagnosis Mission report, the IMF stressed that these reforms would ensure stronger autonomy at the central bank, even though the government remains the sole shareholder of SBP.

Earlier, in 2022, Pakistan revised the SBP Act due to pressure from the IMF, granting complete independence to the central bank and removing the finance secretary’s vote on the SBP board.

Currently, the SBP board includes the governor and eight non-executive directors, one from each province. However, two of the three sanctioned deputy governor posts remain vacant, with only Saleem Ullah serving in finance, inclusion, and innovation.

In the meantime, Finance Minister Muhammad Aurangzeb stated that the government does not intervene in establishing interest rates or exchange rates, which are set by the State Bank of Pakistan. He further mentioned that an IMF evaluation team will arrive in Pakistan during September to discuss a $1 billion loan installment.

oleh admin | Apr 2, 2025 | banking, business, commerce, loyalty programs, money

PNN

Mumbai (Maharashtra), India, April 2: Customer Capital, a firm that focuses on proprietary commerce loyalty solutions,

Bank of Maharashtra

declared a collaboration to launch a special travel platform along with loyalty incentives for

Bank of Maharashtra

cardholders. This partnership between Customer Capital and

Bank of Maharashtra

aiming to improve the value offering

Bank of Maharashtra

Cardholders can enjoy a smooth and rewarding travel booking experience directly via the BANK OF MAHARASHTRA card website and app.

Customer Capital has developed a white-label travel platform called ‘

Tripstacc

This feature permits banks to tailor customer experiences and obtain detailed insights into travel and expenses (T&E), information that cannot be derived from conventional partnership programs. Such capabilities will empower

Bank of Maharashtra

Cardholders can reserve hotels and tickets through a reliable travel website available via the

Bank of Maharashtra

card website and app.

As per a recent study, the loyalty market in India is expected to expand further and could potentially reach $7.92 billion by 2028. Recognizing this significant opportunity, Customer Capital aims to utilize their platform for better understanding and serving Indian consumers. This partnership puts them in an advantageous position to do so.

Bank of Maharashtra

to utilize Customer Capital’s advanced technologies and innovations such as

Tripstacc

, to further boost its operational abilities and gain a competitive advantage.

Govind Sandhu, CEO & Co-Founder of Customer Capital, stated, “We are delighted to announce

Tripstacc

, our captive commerce travel platform for Bank of Maharashtra. This collaboration introduces a distinctive approach that provides numerous advantages to the bank by offering a tailored solution and proposition for its clients. The model will enable

Bank of Maharashtra

deliver greater value to customers, boost involvement and activation, and improve comprehension of travel spending habits thus increasing their proportion of expenditure on travels”

Govind Sandhu also mentioned, “The landscape of India’s loyalty programs is experiencing substantial change, propelled by advancements in technology, artificial intelligence, changing customer preferences, and updated regulatory frameworks. Our aim is to address gaps within the loyalty sector by concentrating on personalized commercial services and have consequently invested in an array of proprietary e-commerce platforms. These can be provided as white-label options for companies aiming to present these directly to their customers. We believe this approach will prove beneficial.”

Bank of Maharashtra

a favored financial ally for its clients.

About Customer Capital:

Customer Capital is an enterprise dedicated to revolutionizing loyalty practices and establishing Loyalty 2.0 through integrated commerce, advanced artificial intelligence technologies, and insights from industry experts. Established in 2022, this firm has developed a range of services designed to turn loyalty initiatives into significant income sources. They specialize in crafting, implementing, and expanding inventive loyalty strategies enhanced by beneficial partnerships. Operating as a comprehensive provider of loyalty management solutions, Customer Capital provides specialized knowledge across various domains such as ecosystem development, accelerator deployment, and technological advancements—this includes their proprietary AI-powered Loyalty Platform along with their Staccs (captive commerce accelerators), which cater specifically to sectors like online travel and e-commerce.

In tandem with targeted advisory support aimed at ensuring these programs resonate deeply with consumers while remaining financially rewarding, Customer Capital utilizes analytics-driven tools and state-of-the-art tech to generate quantifiable benefits for both stakeholders and end-users alike.

(ADVERTORIAL DISCLOSURE: The aforementioned press release has been supplied by

PNN

ANI shall not bear any responsibility for the content thereof.

Provided by Syndigate Media Inc. (

Syndigate.info

).

oleh admin | Apr 1, 2025 | banking, business, controversies, economics, money

Well-known Nigerian entertainer and movie producer Ayo Makun, widely recognized as AY, has voiced his worries about the high service fees charged by commercial banks in Nigeria.

On his X account (previously known as Twitter), AY raised doubts about how banks can consistently report trillions of Naira in quarterly profits amidst Nigeria’s faltering economy.

He contended that certain fees levied on customers are specific to Nigeria and ought to be contested.

He questioned, “How do banks manage to report trillions in profits each quarter despite a struggling economy? We should challenge the minor charges and deductions from our accounts. These fees often have a specific presence in Nigeria. What explains this?”

Provided by Syndigate Media Inc. (

Syndigate.info

).

oleh admin | Mar 28, 2025 | banking, mobile technology, money, payment processing, rules and regulations

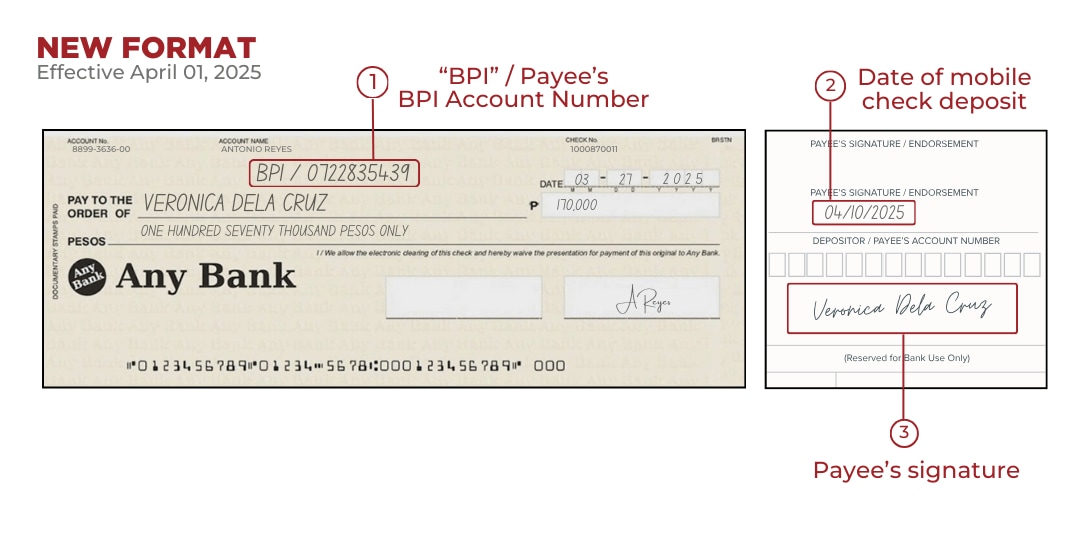

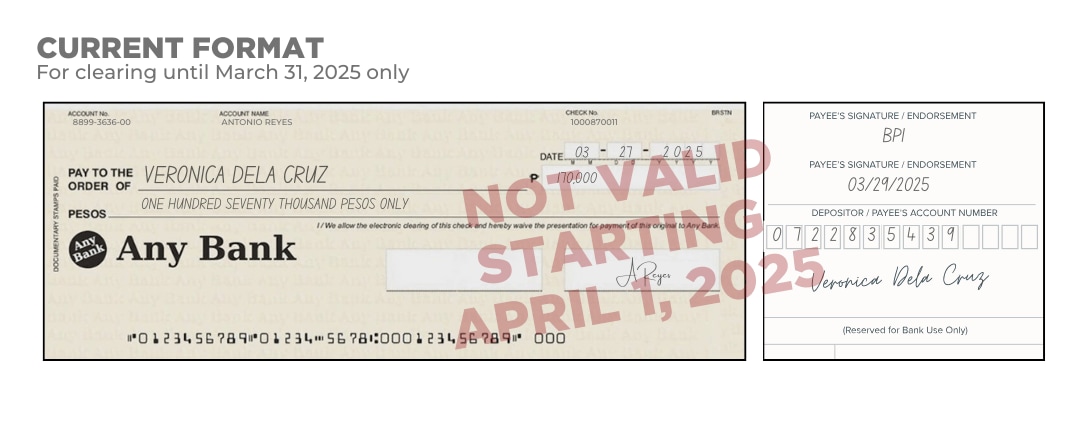

MANILA — The Bank of the Philippine Islands now mandates a revised format for check deposits via its mobile application.

Starting

April 1

Customers planning to deposit their checks digitally should write “BPI/” followed by the payee’s BPI account number above the payee’s name.

Behind the check, they must also include the date of the mobile check deposit along with the payer’s signature.

The previous format mandated that clients write the payer’s account number at the back of the check.

BPI stated that they will process checks in their present form—which looks like what’s depicted below—only up until

March 31.

The bank mentioned that these new rules align with the updated mobile check deposit guidelines set by the Philippine Clearing House Corporation (PCHC).

The lender mentioned that their app’s mobile check deposit feature accepts checks for amounts under ₱500,000.

BPI mentioned that mobile check deposits will follow the same clearing guidelines as those submitted at physical branch locations. Any checks received after 3 PM, on weekends, or public holidays will be handled on the subsequent business day.

BPI reduces InstaPay transfer charges to PHP 10.

RELATED STORY:

![]()

oleh admin | Mar 27, 2025 | banking, business, commerce, financial services, news

-

READ MORE: Bankwest shuts down ALL branches as it discontinues cash services

Staff at a

Commonwealth Bank

Subsidiaries are feeling ‘pressured and overwhelmed’ due to experiencing another wave of significant layoffs within just twelve months.

Since 2022, WA-based Bankwest, operating under the CBA umbrella, has been gradually moving its business clients over to its parent company.

After three years, the initiative has been completed, resulting in 120 employees losing their jobs, while approximately 30 are anticipated to secure new roles within the organization.

This comes after the elimination of 400 positions last year when the bank shut down all its branches and shifted entirely to a digital platform.

The Finance Sector Union has stated that employees are ‘tired of facing an ongoing threat of job loss.’

‘Ever since Bankwest decided to pull out of business banking three years ago, both customers and employees at Bankwest have been dealing with uncertainty,’ stated National Assistant Secretary Jason Hall.

Our members consistently report feeling pressured and overwhelmed across various departments at Bankwest because of the bank’s continuous series of layoffs and overseas outsourcing.

A representative from Bankwest informed Daily Mail Australia that the role of the 130-member transition team was always intended to be temporally restricted.

‘

“The completion of the business banking transition program will affect around 120 positions held by colleagues based in Western Australia,” they stated.

‘[CBA] The group presently has over 100 vacant positions at Bankwest and CBA in Western Australia.’

‘We will collaborate closely with our affected colleagues to assist them in finding new career opportunities within the Group.’

The century-old financial institution shut down 45 of its branches in the previous year.

Fifteen remaining branches based in regional areas were rebranded under Commonwealth Bank.

Every one of the 400 employees at these sites was presented with new job opportunities, and over 300 decided to take them up.

The bank stated further that an additional 500 positions within the CBA Group, focusing on technology, operations, and customer service, will be relocated to WA ‘to aid Bankwest’s shift towards digital transformation’.

“Regrettably, the WA government was misled in this situation—the promise of 500 group positions was made in exchange for Bankwest transitioning entirely to digital operations,” stated Mr. Hall.

He stated that instead, the bank keeps reducing local employment.

‘It’s evident that this commitment was merely an empty pledge made by CBA to deflect criticism for neglecting an entire community.’

‘Members have repeatedly informed us that they feel pressured and overwhelmed across various departments at Bankwest because of the continuous series of layoffs and offshore outsourcing by the bank.’

The union stated they will be sending a letter to WA Treasurer Rita Saffioti requesting an immediate meeting and urging her to promptly address the issue.

The Daily Mail Australia has reached out to Minister Saffioti for their comments.

In 1995, the Western Australian government sold Bankwest to Britain’s Bank of Scotland, which later merged into the London-based Lloyds Banking Group.

In 2008, Lloyds offloaded Bankwest to Commonwealth Bank for $2.1 billion.

CBA extended the Bankwest brand to key eastern seaboard cities as a competitor brand, even though it was under ownership of Australia’s biggest banking institution. However, in 2018, they pulled back to operate solely within Western Australia.

By 2024, approximately 2,100 branches had closed down across various leading banks during a span of six years.

Read more